Ng Gadhiya(Proprietor Namely Niilesh Ghanshyambhai Gadhiya) vs. The State Of Jharkhand And Others

(Jharkhand High Court, Jharkhand)

Heard learned counsel for the parties. The writ petition was preferred with the following relief:

i. “For issuance of an appropriate writ/ order/ direction including writ of certiorari for quashing/setting aside notice dated 14.12.2020 issued in FORM GST DRC-13 by Respondent No.2 (Annexure-8) wherein without following due procedure and without giving any intimation to the petitioner, under Section 79(1) (C) of the Jharkhand Goods and Services Tax Act, 2017 (hereinafter referred as “JGST Act, 2017” for short), the Petitioner's Bank, namely Andhra Bank, Branch- Jagatpura, Jaipur, Rajasthan through Bank Account No.264311100000715 has been directed to pay the GST amounting to Rs. 3814026.24 allegedly due against the petitioner pursuant to the Summary of the Order in Form GST DRC-07 dated 13.10.2020, as being wholly arbitrary and illegal especially in view of the fact that application for rectification of summary of order dated 13.10.2020 as well as appeal of the petitioner is still pending before the Respondents;

ii. For issuance of any other appropriate writ(s)/order(s)/ direction(s) as Your Lordships may deem fit and proper in the facts and circumstances of the case.”

2. Thereafter, an interlocutory application being I.A. No. 601 of 2021 was preferred seeking amendment due to subsequent developments. Petitioner sought addition of further prayer as sub para 3 under para 1 to the following effect:

iii. “For issuance of further appropriate writ/order/direction including writ of certiorari for quashing/setting aside notice dated 15.01.2021 issued in Form GST DRC-13 by Respondent No.2 wherein without following due procedure and without giving any intimation to the petitioner, under section 79(1)(c) of the JGST, the debtor of Petitioner's firm namely, Adani Power (Jharkhand) Ltd. (SEZ Unit) has been directed to pay the GST amounting to Rs.85,65,368.24 allegedly due against the petitioner pursuant to the Summary of the Order in Form GST DRC-07 dated 13.10.2020 and Form GST DRC-07 dated 12.12.2020, as being wholly arbitrary and illegal, especially in view of the fact that application for rectification of summary of order dated 12.12.2020 is still pending before the Respondents.”

3. The matter was heard earlier on 25.03.2021. The order dated 25.03.2021 is extracted herein below:

“Heard Mr. Hardik Vora, learned counsel appearing on behalf of the petitioner along with Mr. Ranjeet Kushwaha, Advocate.

2. Heard Mr. Ashok Kumar Yadav, learned counsel appearing on behalf of the respondent-State.

3. Heard Mr. P.A.S. Pati, learned counsel appearing on behalf of the respondent-GSTN.

4. The present petition has been filed challenging the notice dated 14.12.2020 issued in FORM GST DRC – 13 by respondent No.-2, whereby the petitioner’s banker, namely, Andhra Bank, Branch-Jagatpura, Jaipur, Rajasthan has been directed to pay the GST amounting to ₹ 38,14,026.24 being the dues against the petitioner pursuant to the summary of the order in FORM GST DRC – 07 dated 13.10.2020. As per the writ petition itself, it has been stated that an appeal against the said order was filed on 09.01.2021 with a pre-deposit of amount of ₹ 1,78,222/-. A copy of the provisional acknowledgement for submission of form of appeal has been annexed as Annexure-10 to the main writ petition.

5. During the pendency of the present case, another FORM GST DRC –13 was issued to third party, namely, M/s. Adani Power (Jharkhand) Ltd. (SEZ Unit) dated 15.01.2021 as contained in Annexure-15 for an amount of ₹ 85,65,368.24 and this particular notice was issued inclusive of the amount arising out of summary order dated 13.10.2020. The said notice has been challenged by way of an interlocutory application being I.A. No. 601/2021.

6. It has also been brought on record, by filing a rejoinder to the counter-affidavit of the respondent no. 2, that another appeal has been filed on 02.03.2021 whose provisional acknowledgement for submission of form of appeal has been annexed as Annexure-R8 series with a pre-deposit of amount of ₹ 02,10,703/-.

7. It has been submitted by the learned counsel for the petitioner that for the entire amount which is covered by the notice of attachment dated 15.01.2021, appeals have been filed and provisional acknowledgements have been issued and the appeals were filed within the stipulated timeframe as prescribed under Section 107 of JGST Act. He has referred to the provision of sub-Sections 6 & 7 of Section 107 thereof to submit that once deposit as per sub-section 6 has been made, there is automatic stay of the remaining amount under sub-section 7 of section 107 of JGST Act. The learned counsel has accordingly submitted that in view of the aforesaid provisions of law, garnishee notices which are impugned in the present proceedings may be stayed.

8. The learned counsel further submits that initially in the counter-affidavit filed by the State, it was mentioned that the petitioner had not filed any appeal against the summary of order dated 13.10.2020, but GSTN has filed an affidavit indicating that the said appeal has been filed within the period of limitation on 09.01.2021. The learned counsel submits that accordingly the statement made in the counter-affidavit filed by the State is not correct.

9. Learned counsel for the State, on the other hand, has submitted that the affidavit filed by GSTN is required to be responded and prays for time. He has further submitted that the procedure prescribed under the JGST rules regarding subsequent steps, which were to be taken after filing of the initial appeal, and grant of the provisional receipt of filing of appeal on 09.01.2021, have not been followed and for this affidavit is required to be filed. However, during the course of argument, it is further not in dispute that the appeal filed on 09.01.2021 has not yet been dismissed on account of any non-compliance on the part of the petitioner. So far as the appeal filed on 02.03.2021 is concerned, the learned counsel for the State has submitted that the same is under consideration and the petitioner has taken time and the matter has been adjourned and admittedly, the required amount as per the provisions of Section 107(6) has been deposited.

10. Considering the aforesaid facts and circumstances of the case and in view of the specific provision of sub-Sections 6 & 7 of Section 107 of the JGST Act and in view of the admitted position that the subsequent garnishee notices dated 15.01.2021 covers both the appeals filed by the petitioner, this Court is of the view that on account of pre-deposit which has been made by the petitioner at appellate stage read with the mandate of section 107 (7) of JGST Act, the petitioner deserves an interim protection. The counsel for the State may seek instructions and file response to the affidavit dated 24.03.2021 and also give appropriate explanation for the statement made in the counter-affidavit filed on behalf of respondent No.-2 which prima-facie appears to be incorrect, in view of the affidavit dated 24.03.2021 filed by GSTN.

11. Accordingly, the operation, implementation and execution of the impugned garnishee notice dated 14.12.2020 issued in FORM GST DRC – 13 to the petitioner’s banker, namely, Andhra Bank, Branch-Jagatpura, Jaipur, Rajasthan as well as the impugned garnishee notice dated 15.01.2021 issued in FORM GST DRC – 13 to third party, namely, M/s. Adani Power (Jharkhand) Ltd. (SEZ Unit) as contained in Annexure-15 of the interlocutory application being I.A. 601/2021 are stayed till the next date.

12. The learned counsel for the state is allowed time till 15.04.2021 to file supplementary counter-affidavit in response to the affidavit dated 24.03.2021 filed by GSTN.

13. The matter is adjourned and is directed to be posted on 19.04.2021.”

By the order dated 25.03.2021 the operation, implementation and execution of the impugned garnishee notice dated 14.12.2020 issued in FORM GST DRC - 13 to the petitioner's banker, namely, Andhra Bank, Branch-Jagatpura, Jaipur, Rajasthan as well as the impugned garnishee notice dated 15.01.2021 issued in FORM GST DRC - 13 to third party, namely, M/s. Adani Power (Jharkhand) Ltd. (SEZ Unit) as contained in Annexure-15 of the interlocutory application being I.A. 601/2021 was stayed till the next date.

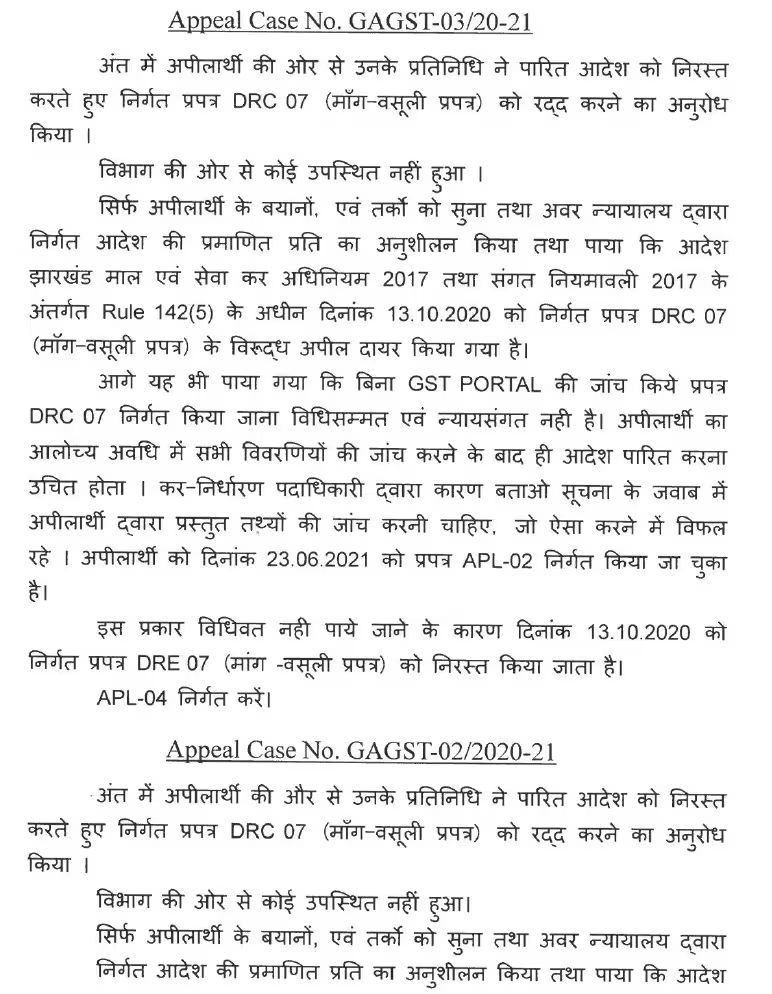

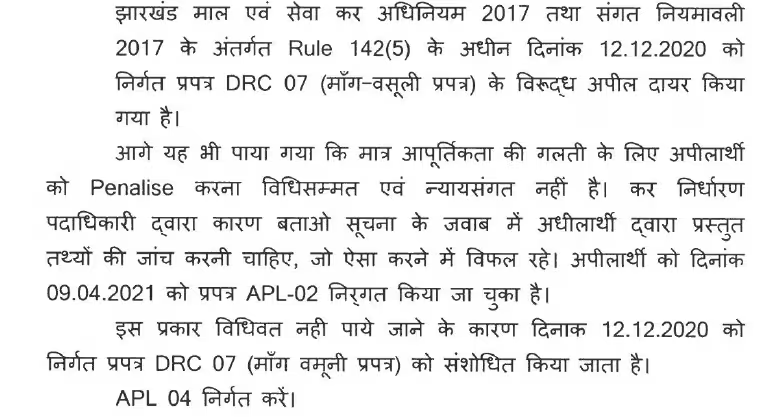

4. Thereafter when the matter was taken up on 23.03.2022, learned counsel for the petitioner Mr. Hardik Vora submitted that both the appeals have been decided in favour of the petitioner under Section 107 of the JGST Act, 2017 upon adjudication. Both the appellate orders have been brought on record by way of supplementary affidavit dated 01.04.2022 with copy to the respondent's counsels. The two appeals being Appeal Case No. GAGST-03/20-21 and Appeal Case No. GAGST-02/2020-21 pertaining to the period 2018-19 and 2019-20 have been decided in favour of the petitioner vide orders dated 01.07.2021 and 19.04.2021 respectively. Petitioner has enclosed the copy of the appellate orders with consequential Form GST APL-04 passed by the learned Joint Commissioner (Appeal), Santhal Pargana Division, Dumka to the supplementary affidavit as Annexure-17 series. The relevant parts of the orders are quoted hereunder:

5. Learned counsel for the petitioner submits that writ petition may be disposed of since no demand notice survives under GST DRC-07 in view of the appellate orders passed in favour of the petitioner.

6. Learned counsel for the respondent State submits that writ petition has become infructuous in view of passing of the appellate orders annulling the demand notice under GST DRC-07. Therefore, the question of recovery pursuant to the garnishee notice under GST DRC-13 dated 14.2.2020 and 15.01.2021 does not arise.

7. We have taken note of the subsequent developments that have taken during pendency of this application. Petitioner has succeeded before the appellate authority and demand notice itself stands set aside. The garnishee notice also therefore does not survive. As such the writ petition has become infructuous. It is disposed of accordingly.