Shakti Marine Electric Corporation. vs. Na

(AAR (Authority For Advance Ruling), Gujrat)

M/s. Shakti Marine Electric Corporation is an authorized wholesale dealer for supply of Combined Wire Rope manufactured by M/s Kadambari Steel Wire Rope Pvt. Ltd and M/s Usha Martin India Limited

2. The applicant has submitted that Combined Wire Rope [Chapter Heading 73121 has got wide usage in General Engineering. Fishing Vessels and also in General Vessels. Presently the applicant is charging 18% GST on the supply made to their Customers. The applicant is mainly operating for supply of Combined Wire Rope in the region of Rajkot. Veraval and Saurashtra having heavy cluster of fishing activities at coastal area like Veraval. Mangrol and District of Kutch.

3. The applicant submits that Customers/Clientele is mainly having Fishing Vessels/Boat and is engaged in fishing activities. The Combined Wire Rope having HSC code 7312 and specification 14mm diameter and construction 6xl9SCF supplied to those Customers for its usage primarily and solely as a part of Fishing Vessels having HSN code 8902.

4. The applicant has submitted that Combination Wire Rope with steel core, stainless steel (red tracer yam) PP-coated combination ropes are used by in trawl fishing all over the world. These ropes also are known as “Taifun Ropes”.

5. The applicant has submitted that the goods of any chapter heading used as a parts of Fishing Vessels having chapter heading 8902 are eligible for 2.5% CGST as per Sr.No.252 of Schedule -I of Notification No. 1/2017-Central Tax (Rate).2.5% SGST vide corresponding Notification issued by Gujarat State Government and 5% IGST Notification No.1/2017-ITR. The said serial number is reproduced as under.

Schedule-I

| Sr.No. | Chapter/ Heading/ Subheading/ Tariff item | Description of goods | Rate |

| 252 | Any Chapter | Parts of the Goods of heading 8901, 8902, 8904. 8905, 8906, 8907 | 2.5% |

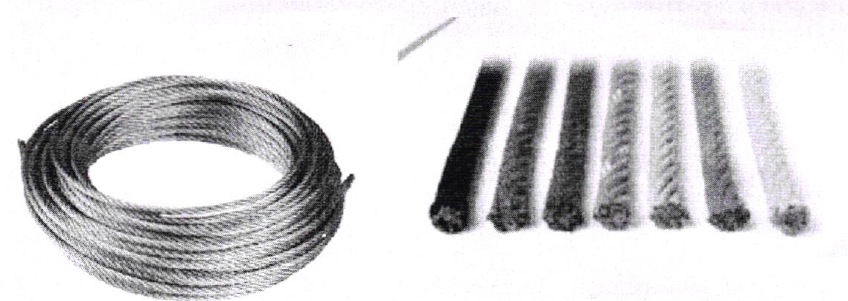

6. The applicant has submitted the Photos of applicant product as follows:

The typical Scanned Image of Combined Wire Rope is as under:

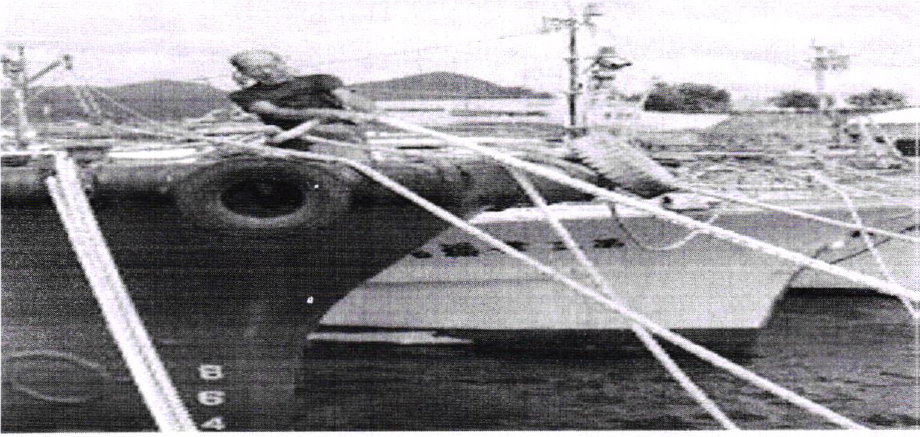

For better understanding the typical images of usage of Combined Wire Rope in Fishing Vessel is scanned and pasted as under.

7. The applicant has further submitted that the following documents against which it has supplied Combined Wire Rope to one of its customer viz Lodhari Ranchod harmat Veraval, who owns Fishing Vessels. It is submitted that it is evident that the Combined Wire Rope is used as parts in Fishing Vessels owned by them.-

i. Invoice No.20GJM 1806/21-22 dated 21.03.2022;

ii. Application addressed to the Assistant Director of Fisheries, Gir Somnath, for availing subsidy;

iii. Certificate of Registry of a Fishing Boat;

iv. Certificate of Licence of a Fishing Boat.

7.1 The applicant further has attached the another sets of the similar documents in respect of the applicant’s other Customer viz. Smt Laxmi Jethalal Gohel. Veraval are also enclosed as under:-

i. Invoice No.20GJM 1361/21-22 dated 25.12.2021;

ii. Application addressed to the Assistant Director of Fisheries, Gir Somnath, for availing subsidy;

iii. Certificate of Registry of a Fishing Boat;

iv. Certificate of Licence of a Fishing Boat.

7.2 The applicant has submits that the Combined Wire Rope supplied are undisputedly used as parts of Fishing Vessels by the customer who are owning Fishing Vessels.

8. The applicant submits that Combined Wire Rope supplied to the Customers owning Fishing Vessels are used as parts of Fishing Vessels; be it for maintenance, manufacture of Fishing Vessels or for modernizing the Fishing Vessels and accordingly they are eligible to avail 5% GST on the Wire Rope supplied by them to such customers. Nevertheless perusal of the said Sr.No.252 of Schedule – I reveals that it does not stipulates any other condition except that goods of any chapter heading is used as parts of chapter heading 8901. 8902, 8904. 8905, 8906. 8907.

9. It is submitted by the applicant that in the given case Fishing Vessel owned by lite applicant’s Customers are classifiable under CITI 8902.00.10 of the First Schedule to the Customs Tariff Act. 1975, the said heading is reproduced as under.

| 8902 | FISHING VESSELS; FACTORY SHIPS AND OTHER VESSELS FOR PROCESSING OR PRESERVING FISHERY PRODUCTS |

| 8902 00 | – Fishing vessels; factory ships and other vessels for processing or preserving fishery products: |

| 8902 00 10 | — Trawlers and other fishing vessels |

| 8902 00 90 | — Other |

9.1 Further, Sr.No.247 of Schedule-1 of the Notification 1/2017-Central Tax (Rate) prescribes that the “Fishing Vessels; factory ships and other vessels for processing or preserving fishery products” classifiable under Chapter Heading 8902 are attracting 5% [2.5% CGST+ 2.5% SGST] and Sr.No.252 of Schedule-I of the said notification prescribes that “goods of any chapter” if used as ”parts of the goods of heading 8902” is also attracting 5% [2.5% CGST+ 2.5%SGST].

Rope is basic parts of Fishing Boat.

10. The applicant submit that there is difference between Vessels and Fishing Vessels. As the very name suggests. Fishing Boats/Vessels has a specific purpose i.e. of Fishing for which usage of. Fishing net is must. The fishing net is tied and hooked with Fishing Vessels with the help of Combined Wire Rope.

10.1 The basic parts of Fishing Boat are available for reference is downloaded from https://www.galatiyachts.com/yachting-news/parts-of-a-fishing-boat-valhalla-boatworks- center-console/ is scanned and pasted as under.

The Basics | Parts of a Fishing Boat

You may already know the basic terminology of a boat and if so, you are already one step ahead Let s go over some of the common parts of a fishing boat mentioned below

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10.2 It is submitted by the applicant that it can be seen that Rope is very much essential for the Fishing Boat. Further. Chapter -4 having title “Design and operation of trawls” published by ICAR-Central Institute of Fisheries Technology, Matsyapuri attached herewith clearly shows how the Combined Wire Rope is used in the Fishing Vessels to tie Fishing Net with the Fishing Vessel. The said chapter explain in detail the role of Rope and, fishing net for Trawl (Trawl is a act of fishing) is essential in the Fishing Boat/Vessels. Thus, it is crystal clear that without Rope, fishing net cannot be used for fishing purpose with the Fishing Vessels. Therefore, to construed Fishing Vessels, the Rope is very much essential part. As submitted above it is clear that Combined Wire Rope is a part of Fishing Vessels, it is therefore applicant’s view that the Sr.No. 252 of schedule-I of the notification is very much applicable when Combined Wire Rope is used as parts of Fishing Vessels and not otherwise.

10.3 In this regard the applicant relies on the Circular No. 52/26/2018-GST, dated 9-8-2018 issued from F. No. 354/255/2018-TRU (Part-2), issued by Government of India. Ministry of Finance (Department of Revenue), Central Board of Indirect Taxes & Customs. New Delhi wherein at para 10.1 and 10.2 it is clarified as under.-

10.1 Applicability of GST on marine engine: Reference has been received seeking clarification regarding GST rates on Marine Engine. The fishing vessels are classifiable under heading 8902. and attract GST @5%, as per S. No. 247 of Schedule-1 of the notification No. 1/2017-Central Tax (rate), dated 28-6-2017. Further, parts of goods of heading 8902. falling under any chapter also attracts GST rate of 5%, vide S. No. 252 of Schedule I of the said notification. The Marine engine for fishing vessels falling under Tariff item 8408 1093 of the Customs Tariff Act, 1975 would attract a GST rate of 5% by virtue of S.No. 252 of Schedule-1 of the notification No. 1/2017-Central Tax (Rate), dated 28-6-2017.

10.2 Therefore, it is clarified that the supplies of marine engine for fishing vessels (being a part of the fishing vessels, falling under tariff item 8408 10 93 attracts 5% GST.

10.4 Though the aforesaid circular is clarification for “Marine Engine” used for Fishing Vessels, the ratio of the said circular is applicable in the applicant’s case as the Wire Rope supplied by the applicant is used as part of Fishing Vessels.

11. The applicant has relied upon the judgment of The Hon’ble Supreme Court of India wherein it have laid down the test to ascertain what is parts in case of Saraswati Sugar-Mills v. Commissioner of Central Excise Civil Appeal No. 5295 of 2003, decided on 2nd August, 2011 [2011 (270) E.L.T. 465 (S.C.)] Hon’ble Supreme Court of India observed:-

11. The meaning of the expression ‘components’ as defined in the dictionary is accepted and adopted by this Court in the case of Star Paper Mills v. Collector of Central Excise – (1989) 4 SCC 724 = 1989 (43) E.L.T. 178 (S.C.); and the same is quoted with approval in CCE v. Allied Air Conditioning Corporation – 2006 (202) E.L.T. 209 (S.C.).

12. In order to determine whether a particular article is a component part of another article, the correct test would he to look both at the article which is said to be component part and the completed article and then come to a conclusion whether the first article is a component part of the whole or not. One must first look at the article itself and consider what its uses are and whether its only use or its primary or ordinary use is as the component part of another article. There cannot possibly be any serious dispute that in common parlance. components are items or parts which are used in the manufacture of the final product and without which, final product cannot he conceived of.

13. The meaning of the expression ‘component’ in common parlance is that component part of an article is an integral part necessary to the constitution of the whole article and without it. the article will not be complete’.

14. This court, in Star Paper Mills (supra) has made a settled distinction while considering whether paper cores are ‘components ‘ in the manufacture of paper rolls and manufacture of paper sheets. It is stated that paper cores ‘ are component parts in so far as manufacture of roll is concerned, but it is not ‘component part’ in the manufacture of sheets. It is useful to quote the observations made by this Court:

“Paper core would also be constituent part of paper and would thus fall within the term “component parts” used in the Notification in so far as manufacture of paper in rolls is concerned. Paper core, however, cannot be said to be used in the manufacture of paper in sheets as component part.

15. In Modi Rubber Ltd. v. Union of India, (1997) 7 SCC 13. the appellant had set up tyre and tube manufacturing plant and imported various plants and machineries. While using the plants and machineries. PPLF (Polypropylene Liner Fabric) was used as a device in the form of liner components to various machinery units to protect the rubber-coated tyre fabric from atmospheric moisture and dust. This Court held that the PPLF was not a component of the machine itself. It was not a constituent part. It was used as a Liner Fabric not only in tyre production but also in similar other industrial processes

12. The applicant has submitted that the test laid down by the Hon’ble Supreme court to determine what is component or part of an article in the aforesaid case is clearly applicable in the instant case. The Combined Wire Rope which constitutes its essential nature without which Fishing Vessels cannot function for Fishing activities in other words without which Fishing Vessels cannot be manufactured and is an integral part of the Fishing Vessels.

13. The applicant has placed reliance on the various Ruling delivered by Authority of Advance Ruling across the country where in it was categorically held that goods of any chapter heading when used as a parts of heading 8901, 8902. 8904. 8905. 8906, 8907 are eligible for 5% Rate of GST in terms of Sr.No.252 ibid. The applicant would like to rely on following Rulings.-

(i) In the case of Excide Industries Ltd. the applicant’s question was “Whether the supply of batteries by the required applicant for the use in warships such as submarines of the Indian Navy falls under Entry 252 of Schedule I to Notification No. 1/2017-Integrated Tax (Rate), dated 28-6-2017 and hence is taxable @ 5% GST?” The Authority of Advance Ruling, Maharashtra Answered in affirmative in their Order No. GST-ARA-39/2020-21/B-58, dated 99-2021 in Application No. 39 reported at 2021 (55) G.S.T.L. 195 (A.A.R. – GST-Mah.)

Here it is pertinent to note that Batteries does not having exclusive use in the Warships. however when it use as a part of warships, it was ruled by he Authority that the applicability of Sr.No.252 of the notification ibid comes in to play.

(ii) In the case of S R Propellers Pvt. Ltd. the applicant, the question was Whether the rate of tax applicable is 5% on commodities such as marine propellers, rudder set, stem tube set, propeller shaft and couplings used only for the purpose of the fishing or floating vessels? The Authority for Advance Ruling, Karnataka in their order KAR ADRG 78/2019, dated 24-9-2019 reported at 2019 (31) G.S.T.L. 382 (A.A.R. – GST) has ruled that “The concessional rate of 5% GST in terms of Entry Number 252 of Schedule I to the Notification No. 01/2017-Central Tax (Rate), dated 28-6-2017 is applicable to the products marine propeller, rudder set, stern tube set, propeller shaft and MS couplings subject to the condition that the said parts form parts of goods falling under 8901, 8902, 8904. 8905, 8906 8907.”

Here it is pertinent to note that marine propellers, rudder set, stem tube set, propeller shaft and couplings does not having exclusive use in the Fishing Vessels, however when it use as a part of warships, it was ruled by he Authority that the applicability of Sr.No.252 of the notification ibid comes in to play.

(iii) In the case of Gurudev Metal Industries, the applicant the question was “Propeller, Shaft/SS Rod, Gun Metal Bush/Bearing, Stuffing Box, Brass Tube/SS tube. Rudder shaft and blade. Sea cork/Water strainer, GM Gate Valve, MS Pipe, Propeller Nut/GM Nut, Coupling, SS Rods & Square, SS Fiat, GM Gland and Ring and MS Plate used in fishing or floating vessels? The authority for Advance Ruling Kerala in their order Advance Ruling No. KER/50/2019, dated 15-7-2019 reported at 2019 (28) G.S.T.L. 191 (A.A.R. – GST) has ruled that “Propeller. Shaft/SS road. Gun metal bush/bearing, Stuffing box. Brass Tube/SS Tube, Rudder Shaft and Blade, Sea Cork/Water Strainer, GM Gate Valve, MS Pipe, Propeller Nut/GM Nut. Coupling, SS Rods Square, SS Flat, GM Gland and Ring and MS Plate used as parts of fishing/floating vessels come under the HSN Code 8902 and are taxable @ 5% (2.5% CGST + 2.5% SGST) under Serial No. 252 of First Schedule of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017 (SRO. No. 360/2017, dated 30-6-2017).”

Here it is pertinent to note that the goods for which ruling was sought for does not having exclusive use in the Fishing Vessels, however when it use as a part of warships, it was ruled by he Authority that the applicability ofSr.No.252 of the notification ibid comes in to play.

(iv) In the case of Techno Tradings and Services (P) Ltd reported at 2019 (24) G.S.T.L. 105 (A.A.R. – GST) following questions were before the Authority for Advance Ruling, Kerala were raised. Applicant is an authorized dealer of Marine Engines and Marine Gear Box used for fishing boats. The question raised by the applicant and Rulings passed by the authority in their order No. KER/34/2019. dated 1-3-2019 as under.-

(a) As per the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017 Marine Diesel Engine falling under TSH 8408 of Customs Tariff Act. 1975, as adopted to GST, attracts 28% IGST (14% CGST + 14% SGST) as per Serial No. 115 of Schedule IV is correct or not?

The Diesel Engines supplied for use in goods falling under Headings 8901. 8902. 8904, 8905, 8906, 8907 will be deemed to be parts of vessels/goods falling under the above headings and thereby taxable @ 5% GST as per SI. No. 252 of Schedule I of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. If it is used for some other purpose, the applicable tax rate would be 28% GST as per SL No. 115 of Schedule IV of the said notification.

(b) As per the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. Gear Box falling under TSH 8483 of Customs Tariff Act, 1975. as adopted to GST. attracts 28% IGST (14% CGST + 14% SGST) as per Serial No. 135 of Schedule IV is correct or not?

The Gear Boxes falling under TSH 8483 when supplied for use in vessels/goods falling under Headings 8901. 8902. 8904. 8905. 8906. 8907 will be deemed to be parts of such goods and thereby would be taxable @ 5% GST as per SL No. 252 of Schedule I of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. If it is used for some other purpose, the applicable tax rate would be 28% GST as per SI. No. 135 of the said notification.

(c) Whether the Marine Diesel Engine (TSH 8408) and Gear Box (TSH 8483) of Customs Tariff Act. 1975 as adopted to GST can be treated as parts of Headings 8902, 8904. 8905, 8906 and 8907 attracting 5% of IGST (2.5% CGST + 2.5% SGST) as per Serial No. 252 of Schedule I of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017 or not?

The marine diesel engine and gear boxes supplied for use in vessels/goods falling under Headings 8901. 8902, 8904, 8905, 8906. 8907 will be deemed to be parts of such goods and thereby taxable @ 5% GST per Serial No. 252 of Schedule 1 of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. If it is used for some other purpose, the applicable tax rate would be as per their respective TSH 8408 and 8483 at the rate of 28% GST as per SI. Nos. 115 and 135 of the said notification.

It is submitted by the applicant that the authority observed that goods for which ruling was sought for. it is categorically ruled that if the said goods is used for Fishing Vessels it will attract GST @ 5%, however if it is used elsewhere it will attract GST @ of 28%

(v) In the case of DHARSAK. V.P. reported at 2018 (13) G.S.T.L. 426 (A.A.R. – GST) where in the Authority for Advance Ruling. Kerala has held that:-

Parts of Fishing/Floating Vessels – Classification and taxability under GST – Advance Ruling thereon – Various parts such as marine propellers, rudder set, stern tube set, propeller shall and M.S. Shaft for couplings are supplied by applicant specific for use in said vessels and cannot be called general purpose parts – Hence, these are covered under Entry No. 252 of Schedule I of Notification No. 1/2018-C.T. (Rate), and taxable @ 5% – Had these parts been used for some other purpose, these would have been taxable @ 18% as per description – Ruled accordingly – Section 9 of Central Goods and Services Tax Act, 2017. [paras 4, 5, 6, 8]

In this case authority observed that goods for which ruling was sought for, it is categorically ruled that if the said goods is used for Fishing Vessels it will attract GST @ 5%, however if it is used elsewhere it will attract GST @ of 18%

14. The applicant has submitted that the trajectory of all these ruling suggests that it is the usage of goods of any chapter when used as a parts of Fishing Vessels that determines GST rate stipulated in Sr.No.252 of the Schedule-I of the notification ibid.

15. Thus in terms of aforesaid submission, though the Combined Wire Rope having chapter heading 7312 is a parts of general use having many applications, however, it is also used as a part of Fishing Vessels, the applicant is of the view that in such a case in terms of Sr.No.252 of Schedule-I of Notification 1/2017-CTR, corresponding notification issued by Gujarat State and Notification No. 1/2017-1TR the GST Rate of 5% is available in their case.

Question on which Advance Ruling sought:

16. Whether. GST Rate of 5% in terms of Sr.No.252 of Schedule-1 of Notification No. 1/2017-CTR. corresponding notification issued by Gujarat State and Notification No. 1/2017-ITR is applicable in the case “Combined Wire Rope” used as a part of Fishing Vessel?”

Personal Hearing:

17. Personal hearing granted on 08-07-22 and 02-09-22 was attended by Shri R.S.Parmar (Advocate) and he reiterated the submission. Shri Niranjan Singh, Assistant Commissioner, Div-11. CGST Rajkot was appeared on behalf of the Revenue.

Revenue’s Submission:

18. Revenue (Centre) vide letter No. GEXCOM/TECH/GST/1735/2022-TECH-O/o COMMR CGST Rajkot neither submitted its comments as follows:-

On perusal of the application as well supporting documents submitted by the applicant it is observed that the said applicant is a dealer of various companies and engaged in supply of Combined Wire Rope (HSN-7312). They supply the said rope mainly to customers who are engaged in Fishing activities under Certificate of Registry of a Fishing Boat & Certificate of License of a Fishing Boat/vessel, HSN 8902 covers Fishing vessels; factory ships and other vessels for processing or preserving fishery products. The applicant made application for benefit of Sr. No. 252 of Schedule-I of the Notification No. 01/2017-Central Tax (Rate), corresponding Notification issued by the Gujarat Government and want to charge / pay GST on supply of the subject goods @ 5% instead of @18%. Relevant portion of Notification No. 1/2017-Central Tax (Rate) dated 28.06.2017 is reproduced below;

In exercise of the powers conferred by sub-section (1) of section 9 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on the recommendations of the Council, hereby notifies the rate of the central tax of-

i. 2.5 per cent, in respect of goods specified in Schedule I,

ii.————-

iii. ————–

iv. ————–

v. ————–

vi. ————–

appended to this notification (hereinafter referred to as the said Schedules), that shall be levied on intra-State supplies of goods, the description of which is specified in the corresponding entry in column (3) of the said Schedules, falling under the tariff item, sub-heading, heading or Chapter, as the case may be, as specified in the corresponding entry in column (2) of the said Schedules.

Schedule I – 2.5%

| S.No. | Chapter / Heading / Sub-heading / Tariff item | Description of Goods |

| 1 | 2 | 3 |

| 252. | Any chapter | Parts of goods of headings 8901, 8902, 8904, 8905, 8906, 8907 |

From the above it is clear that on supply of parts of goods falling under HSN 8902 shall attract CGST @2.5%. HSN Code 8902 is for Fishing vessels; factory ships and other vessels for processing or preserving fishery products (excluding fishing boats for sport). Further, it is a fact that the Combine Wire Ropes are general uses items, having various uses. The said applicant has submitted various documents in support of their claim and at para 4 of Annexure-B to their application they argued that the fishing net is tied and hooked with Fishing Vessels with the help of Combined Wire Rope and at para 5 of Annexure-B they submitted the Chapter-4 ”Design and operation of trawls” published by the ICAR-Central Institute of Fisheries Technology. Ongoing through the details it is observed that the applicant mainly submitted details downloaded from https://www.galatiyachts.com and argued that Cleat: a robust metal fitting to which you tie or loop a rope is part of fishing boat. On going through the documents submitted by the applicant there is no evidence showing that the subject Combined Wire Rope is exclusively a part of fishing boat / vessel.

Further, in support of their claim they relied on various judgement and on perusal of the said judgments it appears that the said judgement are not squarely applicable to the case in hand since no judgments are related to supply of Combined Wire Rope. It is also submitted that the Fishing Wire Rope doesn’t necessarily comes with Steel Core and moreover Fishing Vessels (HSN 8902) are not equipped with Combine Wire Rope/ Fishing Wire Rope at the time of manufacturing. Also the said applicant failed to produce evidences showing that the subject Combined Wire Rope is exclusively a part of fishing boat / vessel. Hence, it appears that the subject goods supplied by the applicant, are not covered under Sr. No. 252 of Schedule-I of the Notification No. 01/2017-Central Tax (Rate) and corresponding Notification issued by the Gujarat Government and the same attract GST @18%.

FINDINGS:

19. We have considered the submissions made by the Applicant in their application for advance ruling as well as the submissions made by authorised signatory, during the personal hearing proceedings on 2-8-22 before this authority. We also considered the issue involved, on which advance ruling is sought by the applicant, relevant facts & the applicant’s interpretation of law.

20. At the outset we would like to make it clear that the provisions of CGST Act and GGST Act are in ‘“pari materia” and have the same provisions in like matter and differ from each other only on a few specific provisions. Therefore, unless a mention is particularly made to such dissimilar provisions, a reference to the CGST Act would also mean reference to the corresponding similar provisions in the GGST Act.

21. We find that the applicant is supplying the Combined Wire Ropes mainly to such customers having Fishing Vessels/Boat and are engaged in Fishing activities. The main issue here is to decide whether the Combined Wire Ropes is a part of fishing vessel or otherwise.

22. We find that the applicant is Authorized wholesale dealer for supply of Combined Wire Rope manufactured by M/s Kadambari Steel Wire Rope Pvt. Ltd and M/s Usha Martin India Limited. We have referred the Manual for Wire Ropes DOC No. CMD-III/l 855/1 MANUAL issued by Bureau of Indian Standards wherein the technical specifications and usage of Wire Ropes have been given and are reproduced for the ready reference as under:-

IS 1855: 2003 Stranded Steel Wire Ropes For Winding and man-riding Haulages Mines.

IS 1856 : 2005 Steel Wire ropes for Haulage purposes

IS 2266: 2002 Steel Wire ropes for General Engineering Purposes

IS 2365: 1977 Specification for Steel wire Suspension ropes for lifts, escalators and hoists

IS 2581: 2002 Round Strand galvanized steel wire ropes for shipping purposes

IS 2762 : 1982 Specification for wire rope slings and sling legs

IS 13156 : 1991 Sheave pulley blocks for wire ropes

22.1 We have observed from the above that Wire Rope is used in various fields such as Mines, Haulage, General Engineering, lift & escalators and Shipping depending upon the requirement and usage of the field. It is observed that Wire Rope is used in Shipping but in the Manual use of Wire Rope in fishing vessel have not been mentioned. This confirms that Wire Rope has no specific/general use in the fishing vessel.

23. We find that the applicant in the Para-4 of the application has submitted that,

“The fishing net is tied and hooked with Fishing Vessels with the help of Combined Wire Rope”

This clearly shows that Combined Wire Rope is not a part of fishing vessel but it’s one side is used to tie the Fishing Net and other side of Wire Rope tied on the vessel. The main use of Combine Wire Rope in fishing is to tie the fishing net with vessel. Therefore, fishermen required such wire rope for fishing purpose and the applicant supply such Combine Wire Rope to them. Further, as per the use of Combine Wire Rope it is amply clear from the above that it has no use in the fishing vessel but it is used to tie the fishing net.

24. We find that ‘Parts’ are not defined in the CGST Act/ Rules, but in trade Parlance, Parts is define as ‘essential for the main product without which it cannot be completed’ but applicant goods Combined Wire Rope is not an essential parts of fishing vessel and also it is not used in the manufacture of fishing vessel.

24.1 In this regard the applicant has placed reliance on the judgment of Hon’ble Supreme Court of India wherein it have laid down the test to ascertain what is parts in case of Saraswati Sugar Mills v. Commissioner of Central Excise Civil Appeal No. 5295 of 2003. decided on 2nd August, 2011 [2011 (270) E.L.T. 465 (S.C.)] Hon’ble Supreme Court of India observed:-

11. The meaning of the expression ‘components’ as defined in the dictionary is accepted and adopted by this Court in the case of Star Paper Mills v. Collector of Central Excise – (1989) 4 SCC 724 – 1989 (43) E.L.T. 178 (S.C.); and the same is quoted with approval in CCE v. Allied Air Conditioning Corporation – 2006 (202) E.L.T. 209 (S.C.).

12. In order to determine whether a particular article is a component part of another article, the correct test would be to look both at the article which is said to be component part and the completed article and then come to a conclusion whether the first article is a component part of the whole or not. One must first look at the article itself and consider what its uses are and whether its only use or its primary or ordinary use is as the component part of another article. There cannot possibly be any serious dispute that in common parlance, components are items or parts which are used in the manufacture of the final product and without which, final product cannot be conceived of.

13. The meaning of the expression ‘component’ in common parlance is that ‘component part of an article is an integral part necessary to the constitution of the whole article and without it, the article will not be complete’.

The above judgement of Hon’ble Supreme Court of India has clearly defined what the Parts are. The Apex Court has held that Parts are used in the manufacture of the final product/article and is an integral part of the final product and it is must to complete the whole article without it the final product/article will not be complete. The applicant product Combine Wire Rope is not used in the manufacture of fishing vessel and also it is not an essential or integral part of the fishing vessel without which the fishing vessel will not be complete. Whereas the impugned goods is used tie the fishing net with fishing vessel means Combine Wire Rope is necessary for the fishing net.

25. We find that the applicant in Para-4 of the application has submitted the details of basic parts of Fishing Boat downloaded from website https:// www. Galatiyachts.com/yachting-news/parts-of-a-fishing-boat-valhalla- boatworks-center-console/ and in the said list basic parts which are essential to complete the fishing vessel have been mentioned. In the said list one of the basic part is ‘cleat: A robust metal fitting to which you tie or loop a rope’. This means the basic part of fishing vessel is cleat which is used to tie the rope and rope is not a basic parts of the fishing vessel. Therefore, applicant contention that rope is part of fishing vessel is not tenable.

25.1 It is further noticed that the applicant in Para-4 of the application has submitted that, “it is crystal clear that without Rope, fishing net cannot be used for fishing purpose with the Fishing Vessels”. The applicant above submission itself explain that fishing net cannot be used without the Rope, it means that Wire Rope is essential for the fishing net which is used for fishing and without wire rope fishing net will not be of any use. Hence Combined Wire Rope is not the essential/integral part of fishing vessel but it is must for the fishing net.

25.2 We, in view of the discussion hold that the applicant goods Combined wire Rope is not a Part of the fishing Vessel.

26. We. now refer to the entry No. 252 of Notification No. 1/2017-CT (Rate) dated 286-2017 as amended and same is reproduced as follows :

Schedule-I

| Sr. No. | Chapter/ Heading/ Subheading/ Tariff item | Description of goods | Rate |

| 252 | Any Chapter | Parts of the Goods of heading 8901, 8902, 8904, 8905, 8906. 8907 | 2.5% |

As per the said entry Parts of goods of chapter heading 8901, 8902, 8904, 8905, 8906, 8907 attracts CGST @ 2.5%. Fishing Vessel are classified under CTH No. 8902 of Customs Tariff and same is read as under :

| 8902 | FISHING VESSELS; FACTORY SHIPS AND OTHER VESSELS FOR PROCESSING OR PRESERVING FISHERY PRODUCTS |

| 8902 00 | – Fishing vessels; factory ships and other vessels for processing or preserving fishery products : |

| 8902 00 10 | — Trawlers and other fishing vessels |

| 8902 00 90 | — Other |

26.1 The applicant has argued that Combine Wire Rope is a part of fishing vessel and therefore is eligible for the GST rate @ 5 % under entry at Sr. No. 252 of the Not. No. 1/2017-CT (Rate) dated 28-6-2017. We have already discussed in the above paras that Combine Wire Rope is not a part of fishing vessel but it is used to tie the fishing net with the vessel. Therefore, applicant argument does not hold good and Combine Wire Rope is not eligible for the GST Tax @ 5% under entry at Sr. No. 252 of Not. No. 1/2017-CT (Rate) dated 28-6-2017.

27. The applicant has placed reliance on the Circular No. 52/26/2018-GST, dated 9-82018 issued from F. No. 354/255/2018-TRU (Part-2), issued by Central Board of Indirect Taxes & Customs, New’ Delhi wherein at para 10.1 and 10.2 it is clarified that, ‘the supplies of marine engine fishing vessel (being a part of the fishing vessel), falling under tariff item 8408 10 93 attracts 5% GST’. The said clarification is issued with regard to marine engine which is integral part of fishing vessel as such without engine fishing vessel cannot be sail in the sea and without it the fishing vessel will not be completed. Whereas the applicant product viz. Combined Wire Rope is not an integral part of the fishing vessel as already discuss in the above paras of the ruling. In view’ of the discussion the said Circular is not relevant in the instant case.

28. The applicant has placed reliance on the judgment of Supreme Court of India pronounced in the case of Modi Rubber Ltd. v. Union of India, (1997) 7 SCC 13. In the said case, the appellant had set up tyre and tube manufacturing plant and imported various plants and machineries. While using the plants and machineries, PPLF (Polypropylene Liner Fabric) was used as a device in the form of liner components to various machinery units to protect the rubber-coated tyre fabric from atmospheric moisture and dust. The Hon’ble Apex Court held that the PPLF was not a component of the machine itself. It was not a constituent part. It was used as a Liner Fabric not only in tyre production but also in similar other industrial processes.

28.1 The said judgment is not applicable in the instant case as such Hon’ble Supreme Court of India has ruled that PPLF was not a component of machinery and it was used as a Liner Fabric not only it tyre production but also in similar other industrial process. In the instant case Combined Wire Rope is used in various fields like Mines, Haulage, lift & escalators and shipping. Combined Wire Rope does not have specific use in fishing vessel but it has general uses and in the applicant case it is used by the fishermen to tie the fishing net with the vessel for fishing in the sea/lake. Hence applicant goods Combined Wire Rope is not essential/integral part of fishing vessel but it is used in the fishing net for the fishing.

29. We find that the applicant has placed reliance on the following Advane Ruling pronounced by the various authority of Advance Ruling.-

(i) The Authority of Advance Ruling, Maharashtra In the case of Excide Industries Ltd vide Order No. GST-ARA-39/2020-21/B-58, dated 9-9-2021 in Application No. 39 reported at 2021 (55) G.S.T.L. 195 (A.A.R. – GST – Mah.) has answered in affirmative to the question “Whether the supply of batteries by the required applicant for the use in warships such as submarines of the Indian Navy falls under Entry 252 of Schedule I to Notification No. 1/2017-Integrated Tax (Rale), dated 28-6-2017 and hence is taxable @5% GST?”

(ii) The Authority for Advance Ruling, Karnataka in the case of SR Propellers Pvt. Ltd in their order KAR ADRG 78/2019. dated 24-9-2019 reported at 2019 (31) G.S.T.L. 382 (A.A.R. – GST) has ruled that “The concessional rate of 5% GST in terms of Entry Number 252 of Schedule I to the Notification No. 01/2017-Central Tax (Rate), dated 28-6-2017 is applicable to the products marine propeller, rudder set, stern tube set. propeller shaft and MS couplings subject to the condition that the said parts form parts of goods falling under 8901, 8902, 8904, 8905, 8906 & 8907.”

(iii) The authority for Advance Ruling Kerala in the case of M/s Gurudev Metal Industries in their order Advance Ruling No. KER/50/2019, dated 15-7-21 reported at 2019 (28) G.S.T.L. 191 (A.A.R. – GST) has ruled that “Propeller, shaft/SS road, Gun metal bush/bearing, Stuffing box, Brass Tube/SS Tube, Rudder Shafts and Blade, sea Cork/Water Strainer, GM Gate Valve. MS Pipe. Propeller Nut/GM Nut. Coupling. SS Rods & Square, SS Flat, GM Gland and Ring and MS Plate used as parts of fishing/boating vessels come under the HSN Code 8902 and are taxable @ 5% (2.5% CGST + 2.5% SGST) under Serial No. 252 of First Schedule of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017 (SRO. No. 360/2017, dated 30-6-2017).”

(iv) In the case of Techno Tradings and Services (P) Ltd reported at 2019 (24) G.S.T.L. 105 (A.A.R. – GST) following questions were before the Authority for Advance Ruling, Kerala were raised. Applicant is an authorized dealer of Marine Engines and Marine Gear Box used for fishing boats. The question raised by the applicant and Rulings passed by the authority in their order No. KER/34/2019, dated 1-3-2019 is as under :-

(a) As per the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017 Marine Diesel Engine falling under TSH 8408 of Customs Tariff Act, 1975. as adopted to GST, attracts 28% IGST (14% CGST + 14% SGST) as per Serial No. 115 of Schedule IV is correct or not?

The Diesel Engines supplied for use in goods falling under Headings 8901. 8902. 8904. 8905, 8906, 8907 will be deemed to be parts of vessels/goods falling under the above headings and thereby taxable @ 5% GST as per SI. No. 252 of Schedule I of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. If it is used for some other purpose, the applicable tax rate would be 28% GST as per SI. No. 115 of Schedule IV of the said notification.

(b) As per the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017, Gear Box falling under TSH 8483 of Customs Tariff Act. 1975, as adopted to GST. attracts 28% IGST (14% CGST + 14% SGST) as per Serial No. 135 of Schedule IV is correct or not?

The Gear Boxes falling under TSH 8483 when supplied for use in vessels/goods falling under Headings 8901, 8902, 8904. 8905. 8906, 8907 will be deemed to be parts of such goods and thereby would be taxable @ 5% GST as per SI. No. 252 of Schedule I of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. If it is used for some other purpose, the applicable tax rate would be 28% GST as per SL No. 135 of the said notification.

(c) Whether the Marine Diesel Engine (TSH 8408) and Gear Box (TSH 8483) of Customs Tariff Act, 1975 as adopted to GST can be treated as parts of Headings 8902. 8904, 8905, 8906 and 8907 attracting 5% of IGST (2.5% CGST + 2.5% SGST) as per Serial No. 252 of Schedule I of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017 or not?

The marine diesel engine and gear boxes supplied for use in vessels/goods falling under Headings 8901, 8902, 8904, 8905, 8906, 8907 will be deemed to be parts of such goods and thereby taxable @ 5% GST per Serial No. 252 of Schedule I of the Notification No. 1/2017-Central Tax (Rate), dated 28-6-2017. If it is used for some other purpose, the applicable tax rate would be as per their respective TSH 8408 and 8483 at the rate of 28% GST as per SL Nos. 115 and 135 of the said notification.

(v) In the case of DHARSAK. V.P. reported al 2018 (13) G.S.T.L. 426 (A.A.R- GST) where in the Authority for Advance Ruling, Kerala has held that;

Parts of Fishing/Floating Vessels – Classification and taxability under GST – Advance Ruling thereon – Various parts such as marine propellers, rudder set, stern tube set, propeller shaft and M.S. Shaft for couplings are supplied by applicant specific for use in said Vessels and cannot be called general purpose parts – Hence, these are covered under Entry No. 252 of Schedule I of Notification No. 1/2018-C. T. (Rate), and taxable @ 5% – Had these parts been used for some other purpose, these would have been taxable @ 18% as per description – Ruled accordingly – Section 9 of Central Goods and Services Tax Act, 2017. [paras 4, 5, 6, 8]

29.1 It is observed that in all the above Advance Ruling it was held that the goods whenever used as a parts of fishing vessel/vessel it attract 5% GST as per entry No. 252 of Notification No. 1/2017-CT (Rate) dated 28-6-2017 otherwise it will attract applicable GST rate of the goods. The above Ruling are not applicable in the instant case as such the facts and circumstance of this application are not similar to the above Advance Ruling. In the instant case Combined Wire Rope is not a part of fishing vessel but it is used to tie the fishing net with the vessel, therefore all the Advance Ruling are not applicable in the instant case. However, as per Section 103 of CGST Act, 2017, any Advance Ruling is binding on the Applicant who has sought it and on the concerned officer or the jurisdictional officer in respect of the Applicant. Therefore, above cited Advance Ruling cannot be relied upon in the instant case.

30. We, hereby pass the Ruling:

RULING

Combined Wire Rope is not used as a part of fishing vessel and the impugned goods does not cover under entry No.252 of Schedule-I of Notification No. 1/2017-CT(Rate) dated 28-06-2017 as amended and is not eligible to GST @ 5%{ CGST 2.5% + SGST 2.5% and IGST 5%}.