Sri Balaji Transport vs. The Principal Secretary/Commissioner Of Commercial Taxes & Other

(Madras High Court, Tamilnadu)

ORDER

This common order will govern the captioned main writ petition and captioned ‘Writ Miscellaneous Petition’ [‘WMP’].

2. Captioned matter is in the Admission Board today. Mr.S.Vijayakumar, learned counsel for writ petitioner and Mr.C.Harsha Raj, learned Additional Government Pleader (Tax) who accepted notice on behalf of all the three respondents are before this Court.

3. Owing to the limited perimeter within which the captioned matter perambulates, main writ petition was taken up with the consent of both sides and for this very reason, a counter affidavit from the respondents is really not necessary.

4. Short facts shorn of granular particulars are that the writ petitioner transported ‘Carbon Black Feedstock Oil’ [‘CBFS Oil’ or ‘said consignment’ for the sake of convenience]; that the writ petitioner imported said consignment from Singapore by sea; that thereafter it was transported by Rail from Mumbai to Chennai; that in Chennai when the truck was moved by surface, the truck was intercepted on 06.12.2022 at 09.35 a.m at Tondiarpet (Kasimedu); that the truck bears Registration No. TN 32-AE- 9889; that one Deepak, who was in the truck, had given a ‘statement which has been recorded on 06.12.2022 in FORM GST MOV-01, bearing reference O.R.No.142/2022-23 (RS-VI)’ [hereinafter ‘impugned proceedings’ for convenience] and this has been impugned in captioned writ petition; that the impugned proceedings says owner/driver/person incharge but the options have neither been scored off or ticked by the Authority concerned; that the Revenue counsel, on instructions, submits that Deepak was at the wheel (it would be desirable for the respondents to be careful when such options with obliques are available in templates while making order); that proceedings are under Section 129 of ‘The Central Goods and Services Tax Act, 2017’ [hereinafter ‘C-G&ST Act’ for the sake of brevity, convenience and clarity] are underway.

5. Learned counsel for writ petitioner submits that the consignment was transported by truck from the Railway yard to a weigh bridge and the interception occurred during such transit. Adverting to the impugned proceedings, learned Revenue counsel pointed out that only a statement has been assailed and in any event, the interception was owing to the reason that the writ petitioner was not in a position to produce Eway bill. Learned counsel for writ petitioner submitted that E-way bill can be applied for only after weighment at the weigh bridge.

6. Learned Revenue counsel for respondent entered upon a disputation saying that the writ petitioner himself has made an internal weighing and therefore, it is an ingenious but fallacious argument.

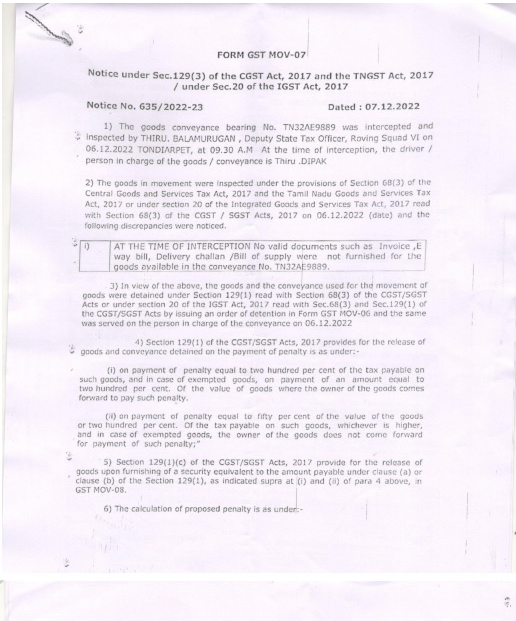

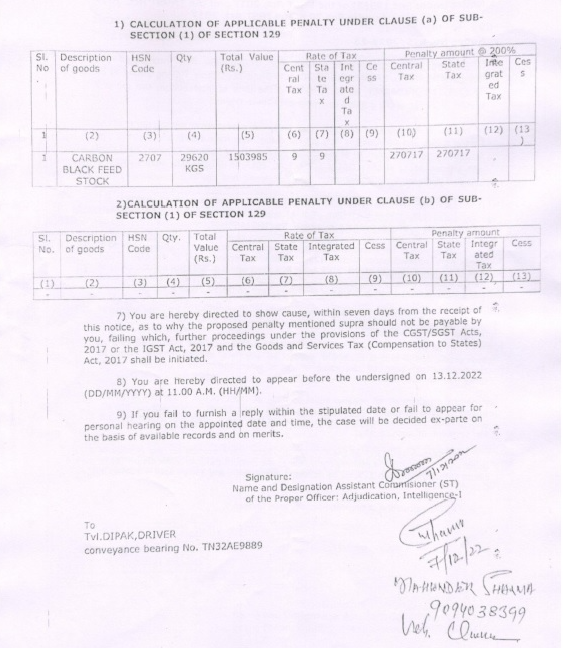

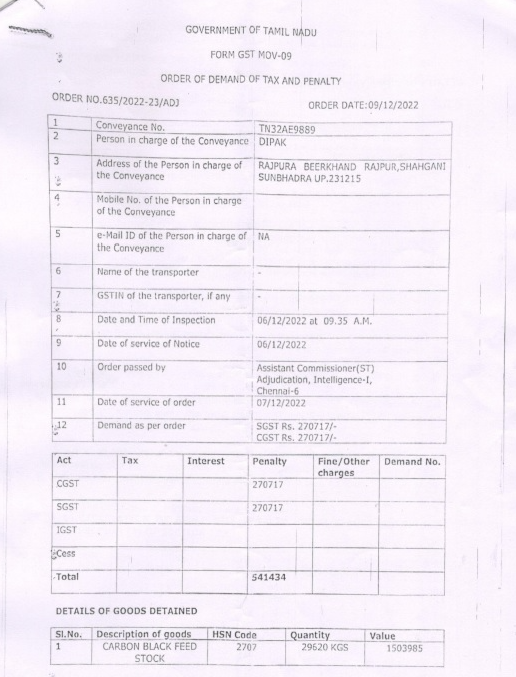

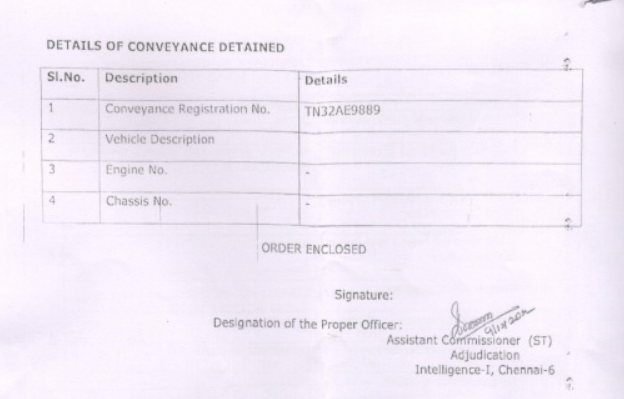

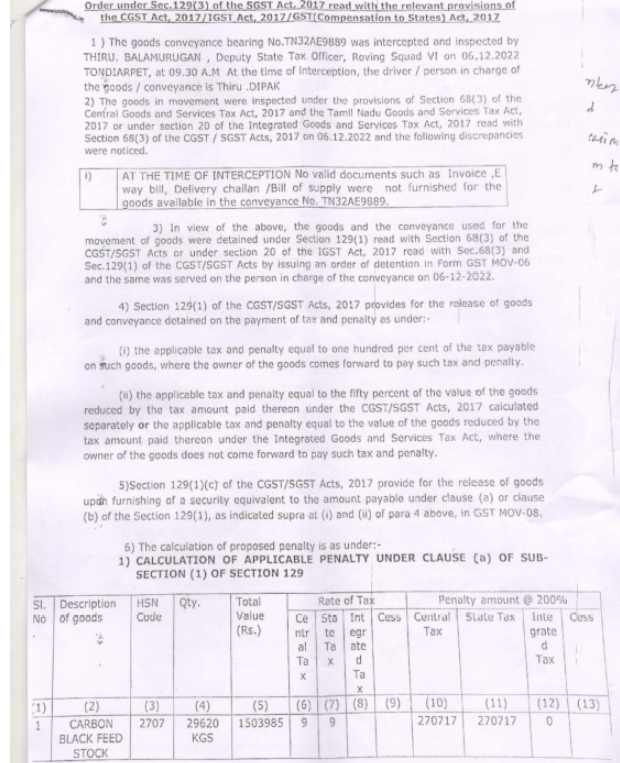

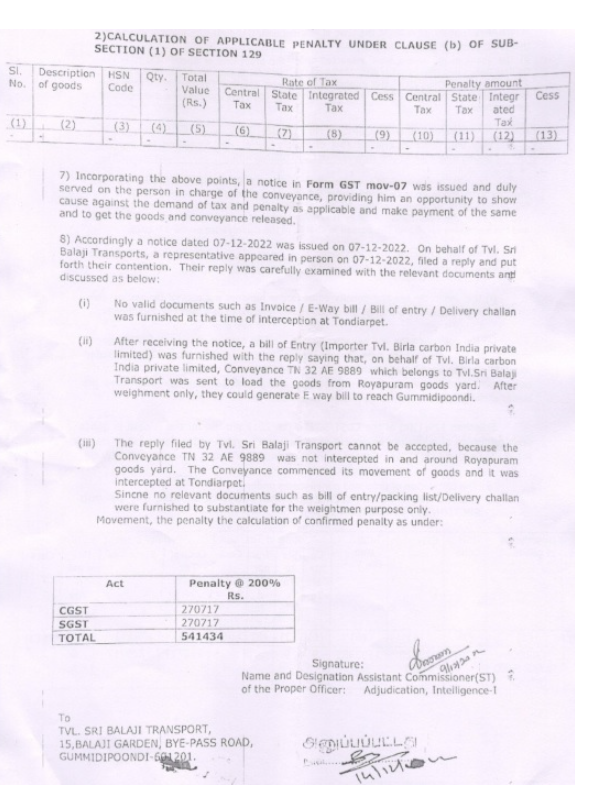

7. In the light of the disputations and contestations, considering that the same turns heavily on facts, this writ Court refrains itself from expressing any opinion or view on the same. There is another reason as to why this writ Court refrains itself from expressing any opinion and proceeds to dispose of the writ petition. That other reason is, learned Revenue counsel, on instructions, submits that pursuant to interception on 06.12.2022, a show-cause notice as statutorily required under Section 129(3) of C-G&ST Act has been issued to the writ petitioner on 07.12.2022, the writ petitioner has sent a reply on the same day, the third respondent has considered the same and has made an order dated 09.12.2022, which has been placed before this Court. A scanned reproduction of 07.12.2022 notice and 09.12.2022 order made by the third respondent are as follows:

8. The matter has been carried to its logical end (to be noted, there is a seven days time line ingrained in Section 129 of C-G&ST Act), it is now too late in the day for the writ petitioner. In any event, the writ petitioner has assailed only a record of statement given by the person at the wheel qua the truck that was intercepted. In this view of the matter, it is now for the writ petitioner to assail the aforementioned 09.12.2022 order bearing reference Order No.635/2022-23/ADJ if so desired and if so advised. To be noted, copy of the 09.12.2022 proceedings has been handed over by the learned Revenue counsel to the learned counsel for writ petitioner today. If the writ petitioner chooses to do the same in accordance with law, the Authority / forum / Court would consider the same on its own merits and in accordance with law untrammelled by any observation in this order which has been made for the limited purpose of disposal of captioned writ petition.

9. Sum sequitur is, the writ petition fails and the same is dismissed. Consequently, captioned WMP is also dismissed. To be noted, dismissal albeit preserving the rights of the writ petitioner is limited to the extent indicated supra i.e., providing a window to the writ petitioner to the limited extent set out supra. There shall be no order as to costs.