Income and Expenditure Account Format Free Sample Excel Download

If you run a society, trust, NGO, school, club, or any organisation whose goal is not profit, you still need a clear report showing whether you had a surplus or a deficit in a year. That report is called an income and expenditure account.

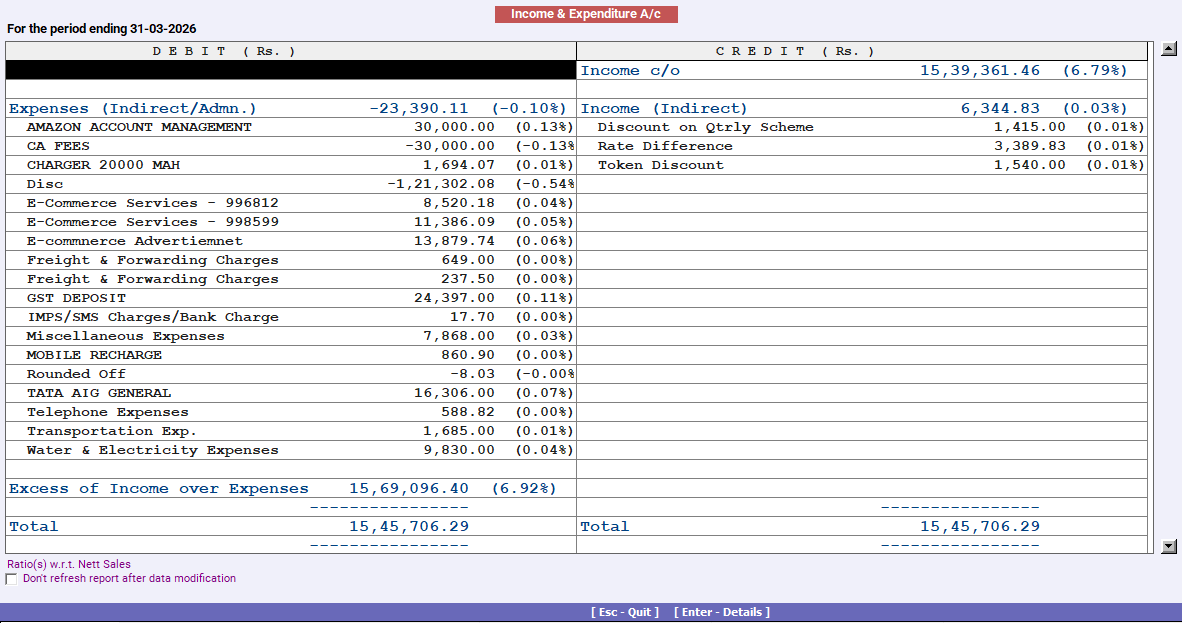

The income and expenditure account format helps you understand surplus or deficit for the year and supports clean reporting for members and auditors. An Excel format is the easiest way to prepare and update it.

India’s No.1 GST Billing & Accounting Software

check_circleLightning-Fast Billing with Barcode scanning

check_circleAuto E-Way Bill & E-Invoicing

check_circleMobile App

check_circleComplete Accounting

check_circleAdvanced Inventory Management

check_circleAuto Payment Reminders

check_circle1-Click GST Filing & Reconciliation

check_circle24*7 support

What is an income and expenditure account format, and who uses it?

An income and expenditure account is like a profit and loss statement, but it is used mainly by non-profit organisations. It is prepared for a fixed period, usually a financial year, and it records income and expenses on an accrual basis. In simple terms, it shows what you earned and what you spent for the period, even if some amounts are still pending receipt or payment. At the end, it shows a surplus or a deficit.

Common users are below:

- Resident welfare associations

- School or college committees

- Charitable trusts and NGOs

- Clubs and associations

- Temples, community groups, and societies

Download the free income and expenditure account format in Excel. Customize it as per your requirement with zero cost.

Income and Expenditure Account Format: What Should Be Included?

A good format of income and expenditure account in Excel usually has these main parts.

Income Side

This includes recurring incomes earned during the period, such as:

- Membership fees and subscription income

- Donations and grants

- Interest received on bank deposits

- Rent income, if any

- Event or program collections

- Any other regular income

This section should also include adjustments like income outstanding and income received in advance, if you track them.

Expenditure Side

This includes recurring expenses for running the organisation, such as:

- Salaries and wages

- Rent, electricity, repairs, and maintenance

- Office expenses and printing

- Event expenses

- Audit fees and legal fees

- Travelling and conveyance

- Depreciation on assets

This section may also include adjustments such as outstanding and prepaid expenses.

At the end, the statement shows:

- Surplus if income is more than expenditure

- Deficit if expenditure is more than income

How Is It Different from a Receipts and Payments Account?

A receipts and payments account shows only cash transactions. It includes everything that was paid or received in cash or bank during the period, even if it relates to previous or next year. It shows income and expenses for the period on an accrual basis. That is why it better reflects the actual year's performance. If you want to know the cash position, receipts and payments is helpful. If you want to know the surplus or deficit for the year, the income and expenditure statement is the right statement.

Common Mistakes to Avoid

- Many organisations wrongly include capital receipts like building funds, corpus funds, or loans received as income. These should not be treated as income in this statement.

- A common mistake is missing accrual adjustments. If you ignore outstanding expenses or pending income, the surplus or deficit can look incorrect.

- Depreciation is often skipped. Even if no cash goes out, it should be included because it reflects asset use during the year.

- People sometimes mix personal or committee member expenses with organisation expenses. Keeping clean heads in Excel helps avoid this.

When Should You Prepare This Statement?

Most organisations prepare it at year's end for audit and reporting. Many also prepare it quarterly to track spending and control budgets. If you want better planning, a simple monthly excel update makes it easier to avoid surprises at year's end.